Getting solar panel insurance was the last thing on my mind when I installed a 5kW system last year.

I watched ₹3.5 Lakhs worth of Tier-1 modules turn into a shattered graveyard of blue glass in just twenty minutes. It wasn’t a fire. It wasn’t a thief. It was a freak pre-monsoon hailstorm in Pune that looked like someone was pelted with stones from the sky. When I called my insurer, they dropped a massive reality check: my “Standard Fire and Special Perils” (SFSP) policy didn’t cover the specific structural failure of the mounting frames. I was staring at a total loss because I lacked proper solar panel insurance for structural damage.

Don’t let that happen to your rooftop setup.

1. The PM Surya Ghar Muft Bijli Yojana Gap

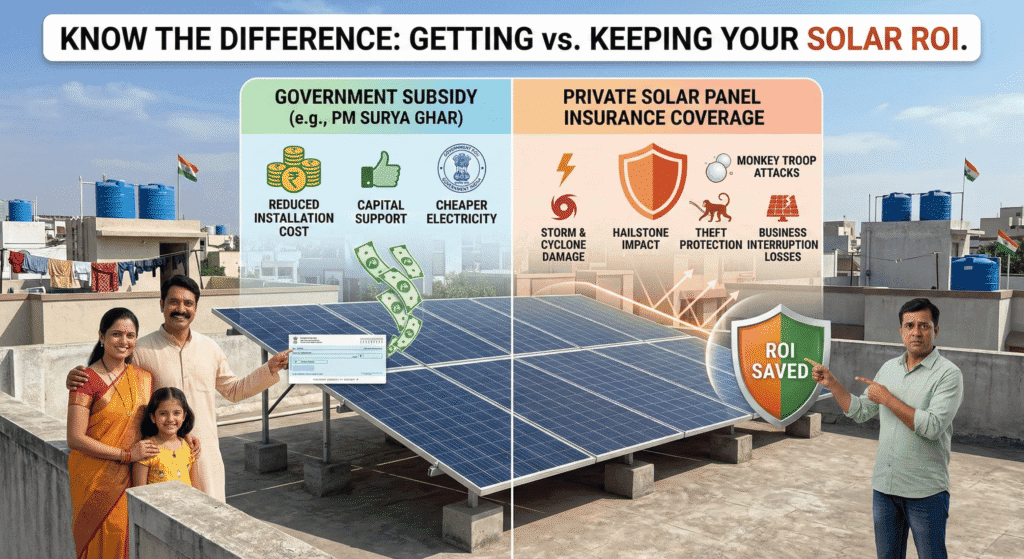

With the push for the PM Surya Ghar scheme, lakhs of Indian homes are going solar. But here is the catch. The government subsidy covers the cost of installation—it does not cover the cost of a monkey troop ripping out your DC cables. This is where specialized solar panel insurance becomes mandatory for peace of mind.

Most homeowners assume the installer’s warranty is the same as solar panel insurance.

It isn’t.

If a monkey in Delhi or a cyclone in Odisha wrecks your array, the installer will just point to the “Act of God” clause in their contract. You need a dedicated solar panel insurance policy that specifically names “Animal Attack” and “Storm/Tempest” as covered perils.

2. Bharat Griha Raksha vs. Standalone Covers

In India, your primary path to solar panel insurance is usually through the Bharat Griha Raksha policy. This is the standard home insurance structure mandated by IRDAI.

But.

You must ensure the “Sum Insured” reflects the current market price of modules from brands like Tata Power Solar or Waaree. If you bought your system three years ago, the replacement cost has shifted. Call your agent. Tell them you have a “Renewable Energy Add-on” for your solar panel insurance needs.

3. The Monsoon & Cyclone Risk Factor

If you live in coastal regions like Andhra Pradesh or West Bengal, your risk profile is insane. High-velocity winds can lift panels right off the pedestals if the grouting isn’t perfect. Standard solar panel insurance must account for these regional atmospheric shifts.

Check your policy for “STFI” (Storm, Tempest, Flood, and Inundation).

I found that many cheap solar panel insurance policies in India cap STFI claims at a fraction of the total value. You want a policy that covers the full replacement of the structure and the modules. And. Make sure it includes the cost of removing the debris. Scraped silicon is heavy and expensive to move.

4. Theft and Vandalism in Rural Clusters

Solar theft is becoming a real headache in outskirts and rural farmhouses.

Copper wiring is a magnet for thieves. While the panels are hard to carry, the inverters (like those from Microtek or Luminous) are prime targets. Any robust solar panel insurance plan in India should include “Burglary and Housebreaking” coverage.

Pro Tip: If your system isn’t fenced or behind a locked gate, some providers of solar panel insurance like ICICI Lombard or HDFC ERGO might reject the claim based on “negligence.”

5. Understanding the “Excess” (Deductible)

In India, we call it the “Compulsory Excess.”

Before the insurance company pays a single Rupee for your solar panel insurance claim, you have to pay the first chunk. For a typical residential setup, this might be ₹5,000 to ₹10,000.

But watch out for “Voluntary Deductibles.” Some agents lower your premium for solar panel insurance by jacking up your out-of-pocket cost to ₹25,000. If a single panel breaks (costing ₹15,000), your policy is effectively useless.

6. Business Interruption for Commercial Rooftops

If you run a small factory or a cold storage unit in Gujarat, your panels aren’t just saving money—they are keeping the lights on.

If your system goes down, you’re back to paying ₹9 per unit to the DISCOM. You can actually get “Loss of Revenue” or “Business Interruption” as part of your solar panel insurance. It pays you for the units you couldn’t generate while the system was being repaired. This makes solar panel insurance a financial lifeline for C&I (Commercial and Industrial) users.

7. How to File a Claim (The Indian Way)

I learned that Indian adjusters are obsessed with “Surveyor Reports.” When your system breaks and you need to use your solar panel insurance:

- Do not move the broken glass immediately.

- Take a video of the damage while it’s still raining/blowing.

- Keep the original invoice and the MNRE-approved components list handy.

- Call the solar panel insurance toll-free number within 24 hours.

Documentation is your only weapon. Without it, you are just someone begging for a payout.

The Survival Checklist

- Mention the solar array in your Bharat Griha Raksha policy.

- Confirm “STFI” coverage for monsoon protection in your solar panel insurance.

- Check if your inverter is covered for “Short Circuit” damage.

- Verify the “Compulsory Excess” amount for your solar panel insurance plan.

So, is your investment actually safe?

The next monsoon doesn’t care about your “Carbon Neutral” certificate. It only cares about how well you’ve hedged your risk with solar panel insurance. Go find your policy papers right now.

For more technical details on Indian energy standards, visit the Ministry of New and Renewable Energy (MNRE) or check the IRDAI website for solar panel insurance guidelines.

Check out our previous blog on 5 Insane 1kW Solar Panel Produces How Many Units? (2026 Secret Guide)